Definition of Accounting

Accounting is a systematic recording day to day business transaction is called as accounting.

Accounting is the process of identifying, recording, classifying and reporting information on financial transactions in a systematic manner for the purpose of providing financial information for decision making.

Identifying:

In accounting, the process begins with identifying financial transactions. This involves recognizing and gathering information about any economic events or activities that have a financial impact on an organization.

Recording:

Once financial transactions are identified, they are recorded in a systematic and organized manner. This typically involves entering data into accounting journals or software.

Classifying:

After recording, transactions are classified or categorized into various accounts. This step involves allocating each transaction to the appropriate account, such as revenue, expenses, assets, liabilities, and equity.

Reporting:

Accounting goes beyond just recording transactions; it involves preparing and presenting financial reports

Types of Accounts

There are basically three types of Accounts maintained for transactions

- Personal Account

- Real Account

- Nominal Account

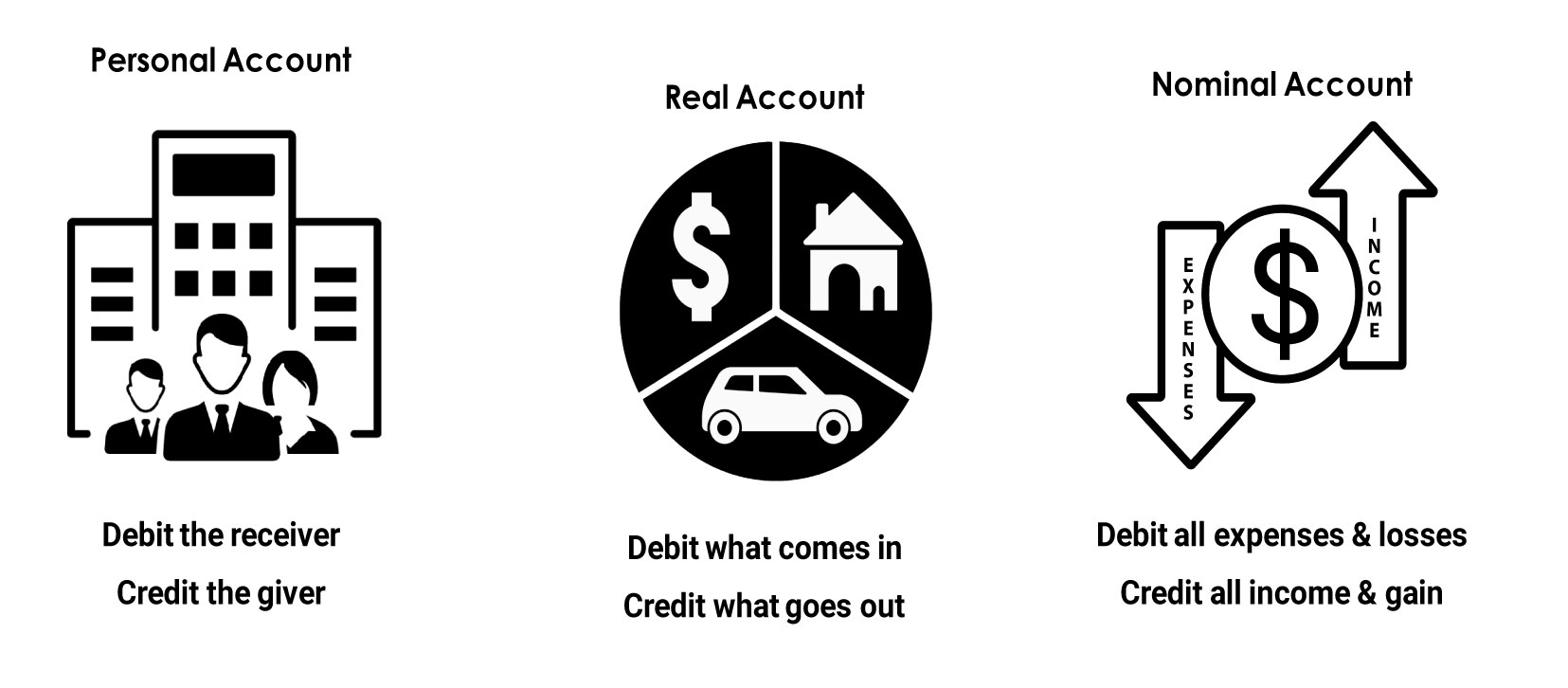

1. Personal Account:

Any individual person or any firms or any company or a bank is considered in a Personal account.

For example:-

- Rajesh Singh

- Munna Enterprise

- Wipro Pvt Ltd

- PNB Bank

- Capital etc.

Rules -:

- Debit the receiver

- Credit the giver

Debit the receiver, credit the giver: When a business receives something, such as cash or goods, it is recorded as a debit in the accounting system. When a business gives something, such as cash or goods, it is recorded as a credit in the accounting system.

2. Real Account:

Account of any physical things. The cash account or goods account are examples of Real account.

For example:-

- Cash

- Land

- Building

- Furniture

- Computer etc.

Rules :-

- Debit what comes in

- Credit what goes out

Debit what comes in, credit what goes out: When there is an inflow of assets or an increase in liabilities, it is recorded as a debit in the accounting system. When there is an outflow of assets or a decrease in liabilities, it is recorded as a credit in the accounting system.

3. Nominal Account:

Account of any invisible things that means that things are in terms of cash are examples of Nominal account.

For example:-

- Discount

- Commission

- Salary

- wages

- Freight etc.

Rules :-

- Debit expenses and losses

- Credit incomes and gains

Debit expenses and losses, credit incomes and gains: This rule states that expenses and losses are recorded as debits in the accounting system, while incomes and gains are recorded as credits.